For this blog post we are focusing on variable selection for our linear regression model. First we must divide the dataset using the code below.

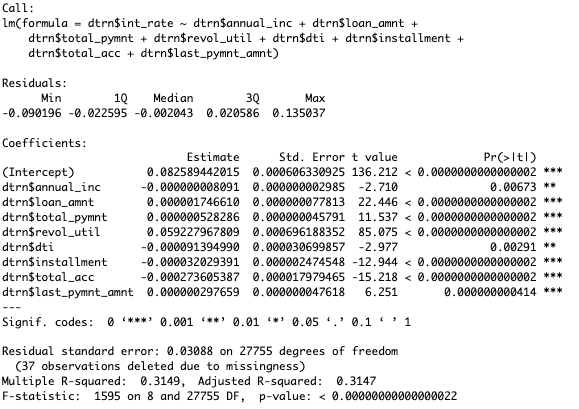

Now, we construct a model to work backwards to select our variables. Since my dataset has 116 variables I just picked the 8 that made logical sense to include. The output of my code is provided below.

CODE:

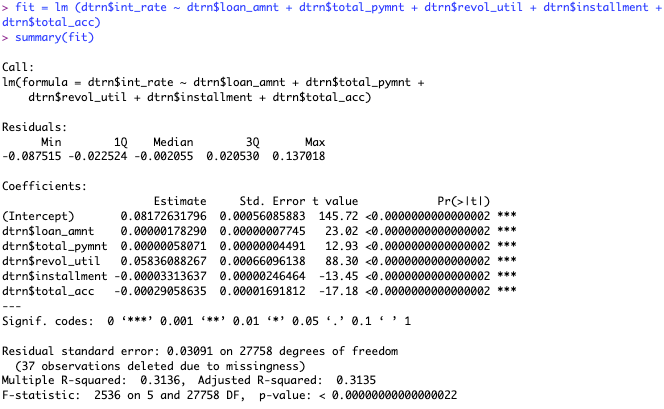

fit = lm (dtrn$int_rate ~ dtrn$annual_inc + dtrn$loan_amnt + dtrn$total_pymnt + dtrn$revol_util + dtrn$dti + dtrn$installment + dtrn$total_acc + dtrn$last_pymnt_amnt)

summary(fit)

I will only take out the least significant variables for my next round. I can also see in my linear regression model that my R- squared value is .3149, this gives us a baseline.

Now all of my variables are significant, but what I didn’t expect was a drop in the R-squared value. The drop is not by much, which most likely helped me because I was overfitting the model. This most likely helped my model be more realistic as I am not using less significant variables. After doing this, I will create my new models with each of the variables in it, creating 16 different models to determine which is the best one. After looking at every single combination, I determined that the one with all of the variables above was the best model based on the R-squared.